The dream is frequently pitched by slick property marketers as a no-brainer: secure a slice of Australian real estate today, lock in current market prices with a modest 10% deposit, and take your time saving money while the developer handles the civil works.

For thousands of Australian property buyers—particularly across the booming growth corridors of Western Sydney, South West Sydney, Hunter Region, and South East Queensland—buying unregistered land off the plan sounds like the ultimate sweet deal.

But beneath the polished master-planned estate brochures lies a complex, highly volatile legal framework. When you buy unregistered land, you are not buying a tangible piece of dirt you can build on tomorrow. You are buying a developer’s legal promise to create a block of land in the future.

If that promise derails due to council delays, civil construction blowouts, shifting planning laws, or developer insolvency, your sweet property dream can rapidly morph into a financial nightmare.

—

The Short Answer: What is the Unregistered Land Trap?

> The Short Answer: Buying unregistered land means purchasing a block of land before its legal title (the individual lot description) has been formally created or registered with the state government. The primary danger is time and volatility. Because months or years pass between signing the contract and final settlement, buyers are exposed to interest rate hikes, falling bank valuations, developer bankruptcy, and contract termination via sunset clauses, leaving them empty-handed in a completely different property market.

—

Registration Delay Risk Snapshot

| Risk trigger | What changes for the buyer | Practical response |

|---|---|---|

| Plan registration slips by 3-6 months | Loan pre-approval can expire before settlement | Request lender policy on re-assessment and keep a finance buffer |

| Interest rates rise before title issue | Borrowing capacity may fall at settlement | Ask the broker to model higher repayment scenarios |

| Valuation comes in below contract price | Extra cash may be needed to settle | Keep savings outside the deposit and avoid maximum borrowing |

Documents To Request Before Exchange

| Document | Why it matters | Who reviews it |

|---|---|---|

| Draft deposited plan | Shows proposed lot shape, dimensions, roads and services | Solicitor or conveyancer |

| Draft Section 88B instrument | Shows easements, restrictions and positive covenants | Solicitor or conveyancer |

| Subdivision approval conditions | Shows what must happen before registration | Solicitor, planner or buyer adviser |

| Finance expiry terms | Shows whether approval survives registration delays | Broker or lender |

Understanding Unregistered Land: The Core Concepts

To safely navigate this market, you must understand the foundational legal difference between a registered block of land and an unregistered one.

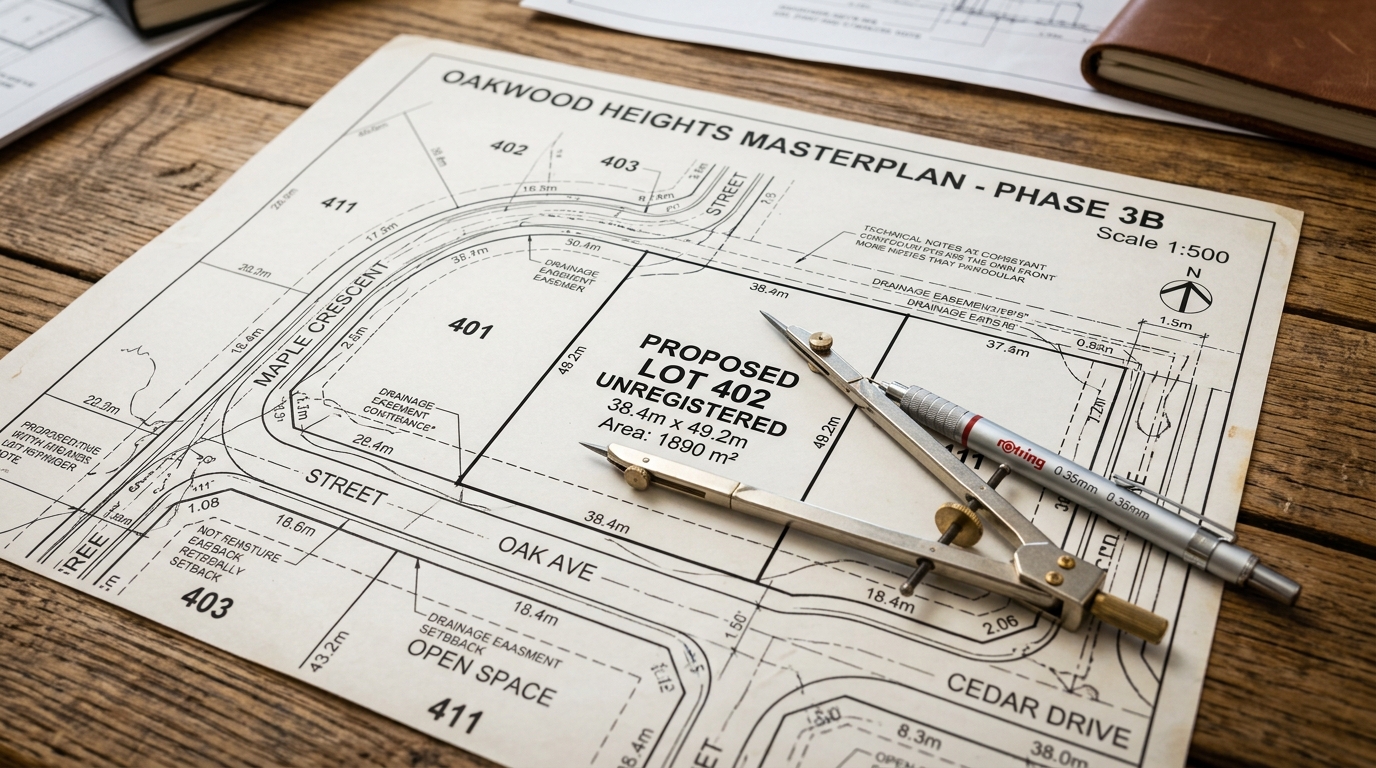

Unregistered Land Meaning

Unregistered land refers to an allotment within a proposed subdivision that exists only on a draft plan. It does not yet possess its own distinct legal identity or reference folio at the state land titles registry.

When you purchase it, you are signing an “off the plan” land contract. The vendor (developer) is legally obligated to complete civil works—such as clearing vegetation, laying asphalt roads, installing electricity sub-stations, and connecting sewer lines—before they can apply to have the final plan registered.

Registered Land vs Unregistered Land

The practical differences between these two states impact your legal rights, your finance structure, and your construction timeline.

| Feature / Metric | Registered Land | Unregistered Land |

|---|---|---|

| Legal Existence | Formally registered with state land title authority. Unique Title reference exists. | Exists only as a proposed lot number on a draft plan of subdivision. |

| Settlement Timeline | Standard 28 to 42 days from the date of contract exchange. | Delayed; usually 14 days after the developer achieves plan registration. |

| Finance Structure | Unconditional bank loan can be formally approved and settled immediately. | Conditional approval only; formal valuation and final approval occur post-registration. |

| Risk Exposure | Low. The land is ready for purchase, valuation, and immediate building approvals. | High. Subject to planning changes, developer insolvency, and sunset clauses. |

| Construction Start | You can submit architectural plans to council or a private certifier immediately. | No building can commence until registration occurs and civil services are live. |

—

Why Buyers Choose Unregistered Land (The Allure)

If the risks are so pronounced, why do thousands of everyday Australians still line up at estate launch days to buy unregistered allotments? The market dynamic thrives on several perceived advantages:

- Buying Time to Save: Buyers only need a 10% deposit at the initial point of contract exchange. The remaining 90% is not due until the land registers, which could be 12, 24, or even 36 months away. This gives first-home buyers an extended window to save additional cash for construction without paying interest on a massive mortgage.

- Locking in Today’s Prices: In a rapidly rising property market, securing a block at today’s fixed valuation means you stand to gain free equity by the time the land registers years later.

- Developer Incentives: Volume builders and developers frequently offer enticing structural rebates, landscaping packages, or stamp duty concessions to off-the-plan buyers to secure the pre-sales required to fund their construction loans.

—

The Major Risks: Why It Can Go Badly Wrong

While the benefits sound highly appealing on paper, the real-world operational journey of an unregistered land development is fraught with friction points.

1. Protracted Registration Delays

Developers routinely underestimate how long civil works and government bureaucracies take. A project advertised to settle in “mid-next year” can easily stretch into the following year or beyond. Delays stem from:

- Unfavorable weather conditions (prolonged rain events stopping civil earthworks).

- Supply chain shortfalls for crucial infrastructure like concrete and electrical conduits.

- Protracted approval bottlenecks with local councils, water authorities, and state planning offices.

2. Finance and Valuation Expiry

This is the single biggest financial trap for everyday retail buyers. When you sign an unregistered land contract, your bank cannot issue an unconditional loan approval because the security asset (the specific title) does not yet exist. Instead, they provide a conditional approval or an “approval in principle.”

These bank assessments typically expire within 3 to 6 months. If your land takes 18 months to register, you will have to re-apply for finance multiple times.

If your personal financial situation changes in that window—if you change jobs, go on parental leave, or if interest rates rise significantly—the bank may refuse to clear your loan when settlement is finally called.

3. Devastating Valuation Shortfalls

If the broader property market cools down during your waiting period, or if the estate fails to hit its premium targets, the bank’s valuer may assess the land as worth less than your agreed contract price upon registration.

Contract Purchase Price: $450,000 Bank Valuation at Registration: $390,000 Shortfall to be paid by Buyer: $60,000

Because banks will only lend a set loan-to-value ratio (LVR) against the *lesser* of the purchase price or the current market valuation, you must make up that entire shortfall in cold, hard cash out of your own pocket. If you cannot produce the difference, you default on the contract, losing your entire 10% deposit, and you can be sued by the developer for damages.

4. Skyrocketing Interest Rates and Building Costs

A lengthy delay between exchange and settlement means you will likely settle your mortgage in a completely different interest rate environment than the one you planned for.

Furthermore, while you wait for the land title to register, building material and labor costs can surge. Fixed-price building contracts signed concurrently with your land purchase often feature expiry clauses of their own. When your land finally registers two years late, your builder may demand an extra $50,000 to execute the build, or walk away completely. For deeper insight into managing unexpected building budget issues, check out our comprehensive breakdown on Hidden building costs in Australia.

5. The Dangerous Sunset Clause Trap

A sunset clause is a vital provision in an off-the-plan contract that sets a definitive calendar deadline by which the developer must register the final plan of subdivision. If registration does not occur by that date, either party can theoretically rescind the contract, returning the deposit to the buyer.

Historically, unscrupulous developers intentionally dragged their heels on civil works to trigger the sunset date. They would rescind the contract, return the buyer’s 10% deposit, and immediately list the exact same block back on the open market for an extra $150,000.

While legislative intervention across various states has significantly curtailed this predatory behavior, the systemic risk remains high. If a legitimate delay occurs and the contract is rescinded, you get your deposit back, but you are forced to re-enter a property market where land prices may have outpaced your savings capacity completely.

6. Forced Material Plan Changes, Easements, and Covenants

When you purchase unregistered land, you are buying based on a *proposed* plan. During construction and council sign-off, things often change.

The local council or water authority might mandate that a major stormwater easement be cut directly across your backyard to manage regional runoff. The developer might need to alter the exact boundary dimensions, reducing your total square meterage or shifting the orientation of your block.

Most off-the-plan contracts contain clauses allowing the developer a margin of error (often up to 5%) in area reduction without triggering a right to compensation or rescission for the buyer. You could end up with a smaller, awkwardly shaped block that cannot accommodate the house design you already purchased. To understand how land restrictions can derail your house configuration, read our detailed guide on Property Easements NSW guide.

7. Critical Infrastructure and Services Delays

Even if the plan gets registered at the land registry, the actual connection of critical modern utilities—including underground electrical grids, mains water, sewer infrastructure, and National Broadband Network (NBN) fiber lines—can face lengthy delays. Without active service connections, your local council will not issue a construction certificate to begin building.

8. The Nightmare of Developer Insolvency

The civil construction sector operates on tight credit margins. If the developer encounters financial distress, goes into voluntary administration, or enters liquidation midway through civil works, the entire project grinds to an immediate halt.

Your deposit is generally held in a secure real estate or legal trust account, meaning you should eventually get it back. However, that legal recovery process can take months or years of stressful litigation. During this time, your capital is locked up, earning minimal interest, while the property market moves out of reach.

—

The Contractual Mechanics: From Deposit to Settlement

Navigating the financial timeline of an off-the-plan land deal requires strict discipline. The transaction unfolds across four distinct phases:

[Phase 1: Contract Exchange] -> Paid 10% Deposit (Held in Trust Account) ↓ [Phase 2: Development Window] -> Civil Works, Council Audits, Title Creation ↓ [Phase 3: Plan Registration] -> Government Authority Issues Individual Titles ↓ [Phase 4: Compressed Settlement] -> Strict 14-Day Window to Pay Remaining 90%

The Transaction Flow Detailed

| Stage | Action Required | Critical Pitfall to Watch For |

|---|---|---|

| 1. Deposit & Exchange | Pay holding deposit (usually 10%) into a joint trust account. Sign and exchange contracts. | Ensure the deposit is held securely in an interest-bearing trust account, not released directly to the developer for working capital. |

| 2. Development Phase | The developer carries out physical site works and seeks final council clearances. | Complete lack of communication or visibility regarding physical civil milestones. |

| 3. Plan Registration | Developer submits final plans to state land registry to create official titles. | The 14-day settlement countdown clock starts ticking the minute registration hits. |

| 4. Settlement | Pay remaining 90% via your lender. Legal ownership transfers to your name. | Severe delays in getting bank valuers on-site, leading to costly late-settlement penalties. |

The Compressed Settlement Pressure Cooker

Once the state land registry approves the subdivision plan, the developer’s solicitor will formally notify your legal representative. This triggers a strict contract countdown—typically giving you exactly 14 days to settle the remaining 90% of the purchase price.

This period is notoriously stressful. Within these 14 days, your bank must dispatch a physical valuer to the freshly registered plot, finalize the internal mortgage paperwork, issue formal loan documents, allow you time to sign them, and coordinate the digital settlement exchange. If your bank slips up and misses the deadline, the developer can charge steep daily penalty interest or cancel the contract entirely, keeping your deposit.

—

State-Specific Legal Protections: Focus on New South Wales (NSW)

Because land administration is managed at the state level, your statutory consumer protection safeguards depend entirely on where the dirt is located.

Sunset Clause Protections in NSW

In response to widespread developer exploitation of sunset clauses, the New South Wales Government introduced strong legislative amendments under the *Conveyancing Act 1919*.

Under these rules, a developer must give you at least 28 days’ written notice before attempting to rescind a contract via a sunset clause. This notice must clearly explain why the land wasn’t registered on time and justify the proposed rescission.

More importantly, the developer cannot automatically rescind the contract unless: 1. You, the buyer, explicitly give written consent to the rescission; or 2. The developer obtains a formal order from the Supreme Court of NSW permitting the rescission.

To win a Supreme Court order, the developer must prove that the delay was outside their reasonable control and that the rescission is fair and equitable to the buyer. This law significantly protects NSW buyers, though it does not completely eliminate the risk of a project failing for genuine reasons.

Disclosure Requirements

Developers in NSW are legally required to attach a formal Disclosure Statement to the front of the contract. This statement must clearly show:

- The proposed lot layout, site dimensions, and orientation.

- Draft plan schedules showing proposed easements or restrictive covenants.

- The sunset date and estimated construction timelines.

If the developer makes a major change to the plan during development that negatively impacts your lot, they must notify you at least 21 days before settlement. If you are significantly prejudiced by the alteration, you may hold a statutory right to rescind the contract and claim your deposit back.

To review official state standards or perform deep-dive verification on a parcel of land, you can use these essential government portals:

- Verify formal land titles, ownership frameworks, and plan rules via the NSW Land Registry Services.

- Review broader title insurance requirements, administrative guidelines, and statutory regulations via the NSW Registrar General.

- Check regional planning rules, zoning maps, and master development requirements across local government areas on the NSW Planning Portal.

- Calculate your upfront state tax liabilities and check concessions for off-the-plan properties via the Revenue NSW transfer duty.

- Track external corporate appointments or search for active administration actions affecting corporate property developers on the ASIC published notices.

—

Crucial Questions to Ask Before You Sign Any Documents

Do not rely on the verbal assurances of a real estate agent or estate project manager. Take a draft copy of the contract of sale straight to an independent property solicitor or licensed conveyancer. Instruct them to evaluate the contract using this targeted question checklist:

Questions for Your Solicitor or Conveyancer

- What is the exact definition of the Sunset Date? Is there a single realistic date, or does the contract contain clauses allowing the developer to automatically extend the sunset window due to ambiguous “inclement weather” or “unavoidable delays”?

- Can the deposit be released to the developer? Ensure the contract strictly mandates that the deposit remains safely inside an independent legal trust account until final settlement.

- What is the allowed margin of error for land area changes? Does the contract allow the developer to shrink the block size by more than 5% without offering any financial compensation?

- What are the consequences if the developer adds new easements? Can I rescind the contract if an ugly sewer main or electrical transformer box is placed directly across my primary building envelope?

Questions for Your Mortgage Broker or Bank Lender

- How long is this specific pre-approval valid for? Will my borrowing capacity be re-assessed from scratch if this estate takes more than 12 months to achieve registration?

- What is your bank’s policy on property valuation shortfalls? Do I have access to emergency capital or alternative loan products if the final valuation comes in significantly under the agreed purchase price?

- How quickly can your valuation team get on-site once registration occurs? Can your internal processing teams comfortably guarantee a full unconditional loan turnaround within a tight 14-day window?

—

Alternatives to Unregistered Land

If the systemic risks of buying an off-the-plan block seem too high for your financial comfort level, you can explore several alternative property pathways:

- Buying Fully Registered Land: This is the cleanest route. The title exists, you can run an instant valuation, settle within a standard 30-day window, and start building your home immediately.

- Established Homes: Buying an existing house eliminates construction wait times and material cost blowouts completely. If you are exploring cost-effective ways to add living spaces down the track, look over our detailed Granny flat NSW approval and costs.

- Prefabricated and Modular Housing: You can purchase an affordable piece of regional land and install a modern factory-built home, which dramatically compresses your build timeline. For a clear look at pricing frameworks, browse our comprehensive Modular homes Australia cost guide.

- Dual Occupancy Developments: Investors looking to maximize yield can target blocks optimized for multiple dwellings. Discover the zoning and planning details in our complete Dual occupancy Australia guide.

—

The Ultimate Final Signing Checklist

Before you authorize your legal representative to exchange contracts and pay your 10% deposit on an unregistered block of land, run through this comprehensive final checklist:

—

Summary

Buying unregistered land remains a legitimate tool for experienced investors and patient home buyers looking to enter the Australian property market. However, it should never be approached as a simple, risk-free shortcut to wealth.

By conducting thorough due diligence, partnering with experienced property professionals, and protecting yourself with strong contract conditions, you can stop the sweet property dream from turning sour.

—